CuorerouC/iStock Editorial via Getty Images

Here at the Lab, we had a good timing rating on Ferrari (NYSE:RACE). Following a rating downgrade (Fig 1), the company released the Q1 earnings, and despite solid results, Ferrari’s total return was negative compared to the S&P 500 changes. As a reminder for our new readers, since early 2022, we have been overweight Ferrari with a publication called RACE Again, recording a triple-digit return.

Mare Ev. Lab Rating Update

Fig 1

Before moving on with our negative takes on Ferrari, I would like to point out that reporting the latest Q1 results is critical. The company closed the first quarter with top-line sales of €1.58 billion, up 10.9% compared to the previous year, and total deliveries of 3,560 units. Cars sold were unchanged compared to Q1 2023. The company reported a record EBITDA of €605 million, signing a plus +12.7% with a margin of 38.2%. This solid operating leverage performance was also recorded in the evolution of EBIT. The adjusted operating profit reached €442 million and was up by 14.8% with a margin of 27.9%. For this reason, net profits reached €352 million, with adjusted EPS of €1.95. On the industrial free cash flow generation, the company reached €321 million in Q1.

Our Negative Takes (Second Part)

Starting with the CEO’s words, Ferrari Q1 “was very positive: revenues and profits recorded double-digit growth with stable deliveries. This was achieved through an even stronger product and country mix as well as a greater contribution from personalizations.” That said, after the Q1 release, the company’s stock price declined by almost 6%. Last time, we reported four negative takes: lower buyback given the >60x implied P/E valuation, lower unit sales in the Chinese region, a negative one-off due to the class action in the United States for the 458 Italia (Ferrari is still an automotive player), and EV uncertainty.

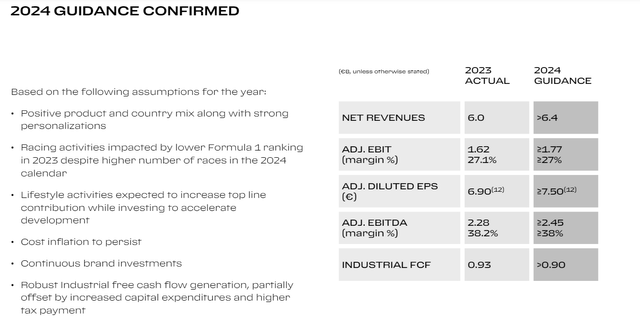

Starting with the latest news, the company confirmed its 2024 guidance. The automotive giant projects net revenues above €6.4 billion, with an EBIT equal to or greater than €1.77 billion and a diluted EPS of at least €7.50. Here at the Lab, we acknowledge solid Q1 results; however, we report few near-term positive catalysts beyond the company’s outlook. We believe Wall Street analysts were projecting a higher 2024 guidance, but we anticipate a valuation priced in. Despite reiterating our long-term positive view on the stock, the company is between two waves of volume growth. On the one hand, volume growth is stabilizing; on the other hand, Ferrari continues to benefit from strong price/mix growth. The usual beat-and-raise dynamic for Ferrari’s rating was not confirmed in the Q1 results. Still, we anticipate a top-line sale and EBITDA margin of €6.55 billion and 29.0% in 2024.

Ferrari Unchanged Outlook

Source: Ferrari Q1 results presentation – Fig 2

Post-COVID-19, our team has been positive in the luxury sector; however, looking at the Q1 earnings season, we have started to see a reset in earnings expectations. Moncler, Brunello Cuccinelli, Hermes, and LVMH were all down despite posting inline or better numbers. For this reason, given the limited catalysts over the near term and the all-time high valuations, investors and Wall Street analysts are likely reducing their holdings. Aside from the expectation of a guidance raise, we believe:

- Ferrari’s order book is normalizing. Looking at the Q1 earnings deck, the company communicated this new normal. Our team sees this normalization in a straightforward way. Ferrari’s brand valuation is due to the car desire of its clientele, and there is a trade-off between desire and waiting periods for customers. We believe there is no concern over Ferrari demand, but the CEO needs to intentionally set higher expectations in the order book. This might provide a jet leg in the Ferrari operating results;

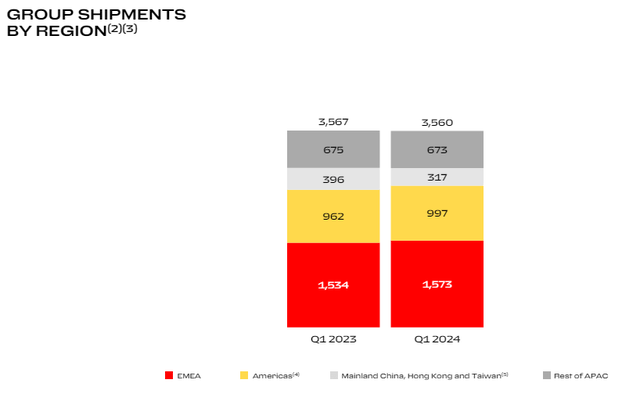

- Looking at the deliveries, Q1 2023 remained the same. That said, as already reported, Continental China, Hong Kong, and Taiwan saw a decrease of 79 deliveries;

- On the conference call, we learned that the company delivered an 80 basis points higher margin thanks to Daytona deliveries in Q1. This number will likely decrease in the upcoming quarter. Ferrari’s margin might be lower than Wall Street’s expectations if we factor in this evolution. This could lead to deteriorating margins in 2024. Again, even if this evolution was already incorporated in our financial estimate, Ferrari will likely be impacted due to the ramp-up phase of the Roma Spider and 296 (Coupe and Spider). These cars are entry-level, weighing on Ferrari’s average selling price. That said, higher selling prices and a better product MIX still support our EBITDA evolution.

Ferrari Order Book Evolution

Fig 3

Risks

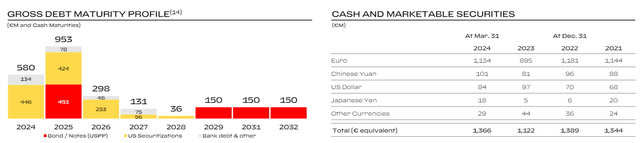

On the downside, there are different risks to consider. Ferrari is not immune to FX risks. In numbers, deliveries outside the EU region account for 1987 units. In addition, as we can see in Fig 5, Ferrari has outstanding debt maturities in 2024 and 2025. We see no problem in refinancing; however, we no longer live in a negative rate interest environment, which might result in a higher cost of debt. Ferrari is an automotive player and is impacted by common business risks such as wage inflation, COGS, and defective auto parts. In addition, there is a risk of higher corporate tax and higher duties tax on luxury goods. Key to the report from our last analysis is the fact that the company “is moving on with new lifestyle activities, such as the Fashion industry. From now on, the company will launch a fashion collection annually for both men and women. This is a new business, and it might fail to meet expectations and the necessary product development.”

Ferrari Deliveries per region

Fig 4

Ferrari Outstanding Debt

Fig 5

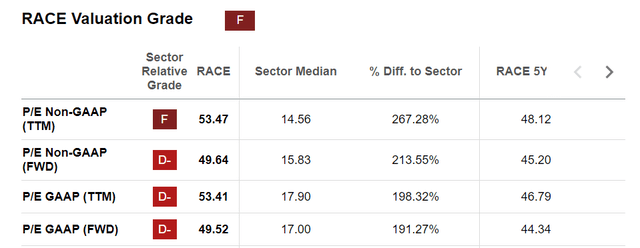

Valuation and Conclusion

Historically, Ferrari has often raised its outlook at the Q2 stage. That said, we are already above the company’s fiscal year core operating profit margin, and the consensus is already there. At this point, we still need to see more evidence of why Ferrari’s margins should increase in 2024. For this reason, we continue to forecast a high EPS of €8.4. We believe incremental buyers are staying on the sidelines, given that the company’s production is covered until 2025. Continuing to value Ferrari aligned with its 5-year historical average at 45x (10% discount compared to Hermes), we reiterate our neutral valuation with a price target of €380 per share and $405 in ADR.

Ferrari SA Valuation

Fig 6

from Finance – My Blog https://ift.tt/OsoxP9R

via IFTTT

No comments:

Post a Comment