artisteer

Overview

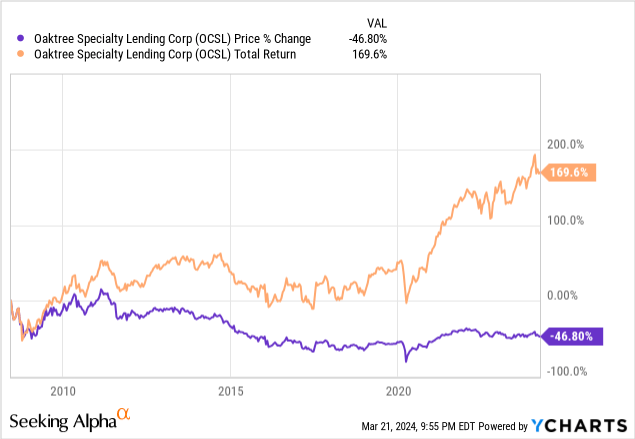

I steadily ignored Oaktree Specialty Lending (NASDAQ:OCSL) as a result of falling share value. I figured that there was no method OCSL had the power to offer a adequate degree of complete return with such a fall in share value. Since inception, the BDC (enterprise growth firm) is down almost 47% in value. Nonetheless, taking a look at complete return since inception paints one other story. Complete return since inception is roughly 170% due to the excessive distributions.

OCSL is a enterprise growth firm specializing in center market financing and debt financing. They earn earnings from the investments they make with debt. It has publicity to a various vary of sectors equivalent to actual property administration, software program providers, healthcare, manufacturing, and totally different joint ventures.

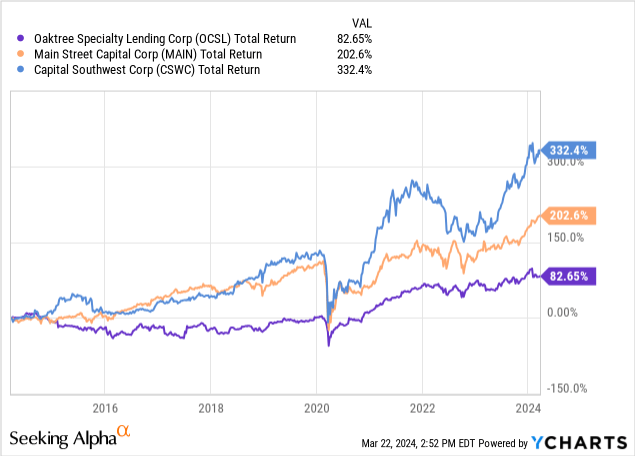

The present dividend yield is 11.3% paid out on a quarterly foundation. Nonetheless, there are already indicators of a dropping of NI (internet funding earnings) that was introduced up on the final earnings name. Plainly this BDC’s portfolio of high quality debt investments differ and may affect NII considerably. Due to this fact I keep cautious of initiating a place. Particularly when there are rock strong different decisions throughout the BDC sector equivalent to Capital Southwest (CSWC) or Predominant Road Capital (MAIN).

Financials & Danger Profile

OCSL reported Q1 earnings lately in February and outcomes have been a bit combined. The NII(internet funding earnings) reported was $0.57 per share and this failed to fulfill expectations by $0.04. $0.57 per share was a lower from This autumn of the prior yr which could be primarily attributed to diminished adjusted complete funding earnings. Nonetheless, this does nonetheless cowl the whole thing of the distribution of $0.55 per share that might be paid on the finish of March.

The diminished funding earnings was attributable to efficiency challenges attributable to 4 of OCSL’s portfolio corporations. Administration has confirmed that they’re working with every of these corporations to deal with every state of affairs independently whereas additionally nonetheless delivering the absolute best end result for OCSL shareholders.

The portfolio corporations which were a supply of points are as follows:

- OTG Administration: an airport concession enterprise that has confronted strain with money stream technology as a result of a better curiosity expense burden due to rising rates of interest.

- Thrasio: an Amazon market aggregator that has confronted challenges with diminished Amazon site visitors and provide chain delays.

- Impel Prescription drugs: A biotech firm that develops central nervous system medication is experiencing decreased gross sales and filed for chapter.

- Singer: The world’s largest stitching machine firm goes by a slowdown because the pandemic.

Whereas OCSL is working by these points, it makes a higher query come up. Is OCSL extra unfastened with their standards in debt investments? Whereas there are solely 4 corporations which are present process points, I can not assist examine this to BDCs which have rock strong strategies of evaluating these corporations. For instance, Capital Southwest has no portfolio corporations which are presently rated on the backside of their analysis scale. I lately printed an article on Capital Southwest which you can learn right here.

OCSL Investor Presentation

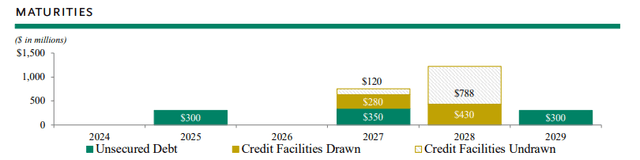

By way of debt maturity, there may be solely $300M of unsecured debt due within the subsequent two years. The vast majority of the affect as a result of maturities is scheduled to happen all through 2027 and into 2028. Administration appears to pay attention to these points on their final earnings name and it is solely a matter of how they execute these modifications and enhancements.

Moreover, we’re carefully monitoring corporations that might want to refinance debt within the coming years as they may face difficulties within the occasion monetary situations grow to be restrictive. In opposition to this backdrop, we consider warning continues to be warranted. Our funding method prioritizes relative worth, drawing upon the complete breadth of Oaktree’s scale and sources to selectively make investments throughout each the sponsor and non-sponsor backed markets as we did within the first quarter, and thoroughly pursue enticing alternatives as they come up. – Armen Panossian, Chief Govt Officer and Chief Investments Officer

Portfolio Development & Challenges

OCSL Investor Presentation

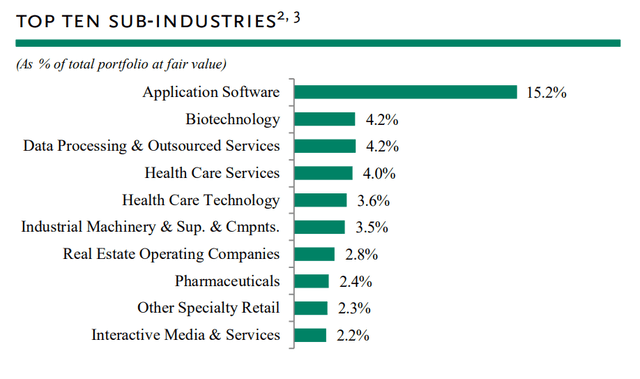

OCSL’s portfolio stays various however has a majority focus throughout the software software program house. Complete investments reached $3B and the portfolio consists of 146 totally different corporations. Their portfolio additionally has a mean weighted yield of 12.2% on their debt investments which is sort of strong.

Over Q1 OCSL had new funding commitments totaling $370M inside their portfolio. These commitments that have been initiated have a weighted common yield of 11.6%. Of this $370M complete, $279M have been in fully new portfolio corporations. As well as, OCSL additionally obtained $214M in money proceeds from just a few totally different sources. This extra capital was a results of debt prepayments, exits, and gross sales. This inflow of capital can now be used to additional develop their funding portfolio and even challenge out a supplemental dividend.

One thing that I like right here is that almost all of their portfolio composition lies inside senior secured debt investments at a floating fee. 78% of their complete portfolio lies inside first lien senior secured debt, totaling $2,351M. 8% of the portfolio additionally consists of second lien senior secured debt, totaling $254M. This leads to the full portfolio being comprised of 86% senior secured debt alongside 84% of the portfolio made up of floating fee debt.

Floating fee debt supplies the potential for elevated returns in a rising rate of interest surroundings which is precisely what we have seen over the course of rate of interest will increase. OCSL holders obtained 4 separate dividend will increase in 2022 as charges started to be elevated. That brings me to debate the dividend!

Dividend & Valuation

As of the newest declared dividend quarterly dividend of $0.55/share, the present dividend yield is 11.4%. The dividend was elevated a number of occasions all through 2022 as charges elevated however the raises might slowly cease now that charges are anticipated to lower later within the yr. As a substitute, administration opted for issuing a particular money distribution of $0.07/share that was paid again in December of 2023.

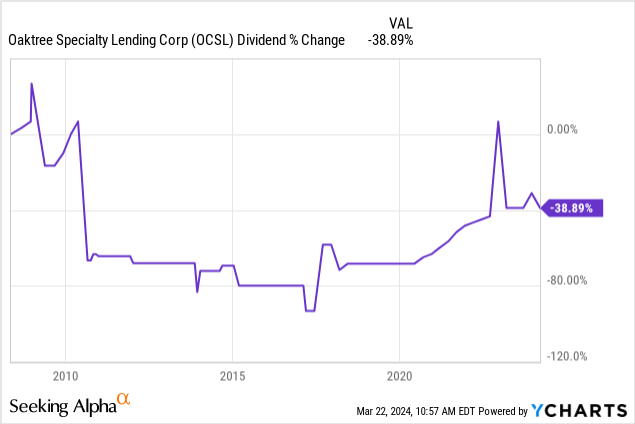

Nonetheless, we are able to see that the dividend has really shrunk since inception. The dividend CAGR (compound annual development fee) over the past 3 years have been insanely robust at 19.48% as a result of larger rates of interest. Nonetheless, over a long term of 10 years the dividend CAGR is adverse at -3.67%.

I perceive that the prioritization of earnings takes entrance seat with regards to BDCs. Nonetheless, I miss out on any advantages right here as there are a number of different BDCs with comparable yield profiles and higher dividend development. Just like the beforehand talked about Capital Southwest, the dividend development has been wonderful for a decade straight. CSWC’s dividend grew at a CAGR of 21.26% over the past ten yr interval! Even Mainstreet Capital’s dividend has delivered dividend development over the past decade with a dividend CAGR of three.89%.

If the beforehand talked about challenges with these portfolio corporations evolve into even nice unfavorable outcomes, the dividend might be threatened. As well as, the annual payout presently sits at $2.20 per share. OCSL’s fiscal yr 2023 complete internet earnings was $2.47 per share. This represents a protection of 112% which is nice! Nonetheless, I consider that future rate of interest modifications mixed with the portfolio challenges can negatively have an effect on complete NII and because of this the dividend might be must be diminished.

By way of valuation OCSL appears to be buying and selling at a premium in relation to the historic worth. Traditionally, the worth traded at a reduction to NAV over the past decade, as you’ll be able to see on the chart beneath. Nonetheless, the current value run has trigger OCSL to now commerce at a slight premium to NAV of 1.1%. This may be attributed to the upper rate of interest surroundings the place BDCs with a debt portfolio of floating charges actually benefitted. The Fed is anticipated to implement 3 totally different rate of interest cuts within the latter half of 2024 and it is seemingly that the worth will fall again to low cost territory.

CEF Knowledge

I wish to finish this with the readability that I do not consider that OCSL is a foul funding for top yield earnings. The BDC has managed to ship earnings and capitalize on this larger fee surroundings as they need to have. My applauds exit to the administration staff for managing the portfolio properly throughout this time-frame and delivering a a number of supplemental distributions to shareholders.

I simply consider that there are higher options that provide comparable excessive yielding earnings with out the chance of challenges inside their portfolio of investments. These challenges might be quick time period buzz however time will inform. Due to this fact, I plan to revisit this BDC as soon as charges have come down a bit. I additionally consider there are higher BDCs which are well-equip to take care of the anticipated rate of interest modifications.

Takeaway

Whereas I feel that OCSL has finished an amazing job at managing the rate of interest challenges and rewarding shareholders accordingly, the present portfolio challenges makes me cautious. I plan to stay on the sidelines and revisit OCSL as soon as rates of interest are reduce. By then I hope that these challenges are resolved or there’s a clearer resolution for these portfolio corporations.

Though the debt portfolio is presently various in nature, I plan to withhold from initiating a place due to the worth buying and selling at a premium to NAV. Traditionally, the worth has traded at a reduction over the past decade and the current run up has modified this, not any basic enhancements. Whereas OCSL has made progress in direction of new commitments, I nonetheless consider there are higher options throughout the BDC house.

from Finance – My Blog https://ift.tt/Qqf4ByP

via IFTTT

No comments:

Post a Comment